Economic Leadership Shift in Southeast Asia: How Vietnam Overtook Thailand

THAILANDVIETHNAM

AI aigov.consulting

10/6/202515 min read

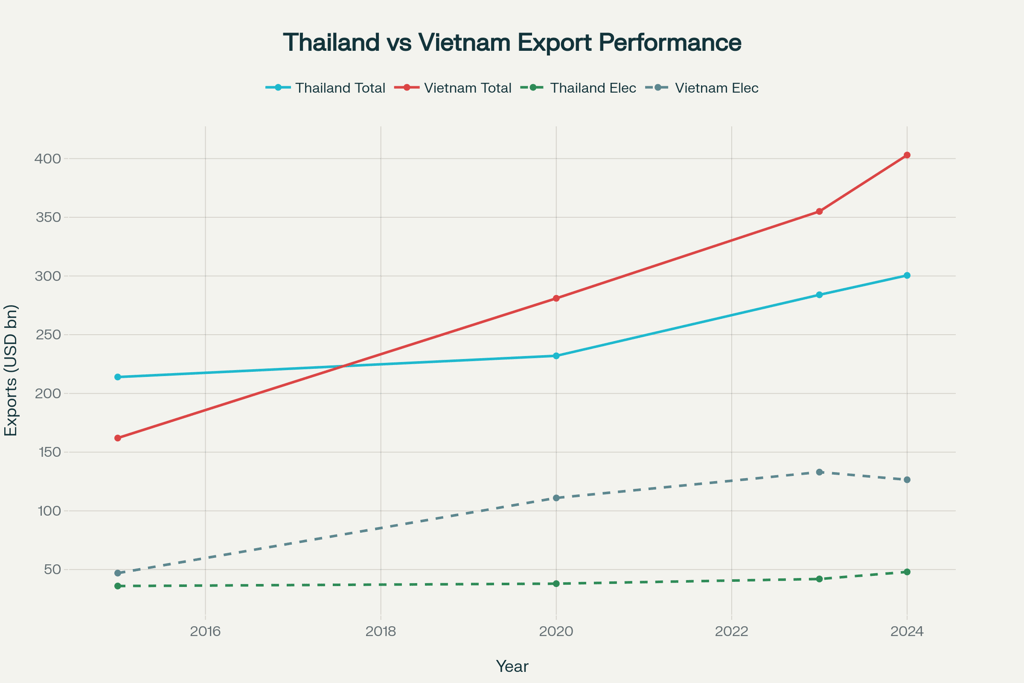

In recent years, Southeast Asia has witnessed a dramatic shift in economic roles that forces analysts to reconsider traditional perceptions of regional hierarchy. Vietnam, once lagging in economic development, has decisively overtaken Thailand in key indicators of export-oriented economy, including total export volume, current account surplus, and economic growth rates. In 2024, Vietnam's exports reached a record 403 billion dollars compared to Thailand's 300.5 billion dollars, while Vietnam's current account surplus amounted to 28 billion dollars compared to Thailand's 13.4 billion. This transformation reflects deep structural changes in the regional economy and demonstrates how strategic reforms, technology investments, and geopolitical advantages can dramatically alter the economic map of the region.

Historical Dynamics and Turning Point

Thailand's Golden Era and Early Signs of Change

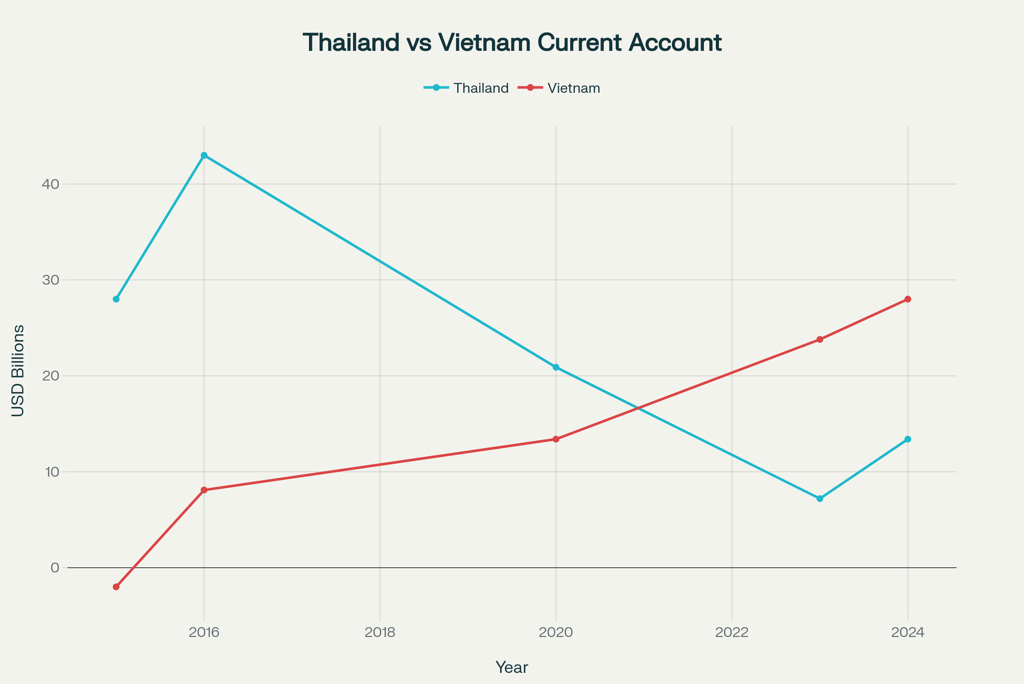

Until recently, Thailand unquestionably dominated the economy of continental Southeast Asia. During the period from 2015 to 2016, the kingdom experienced unprecedented prosperity, demonstrating current account surpluses of 28 and 43 billion dollars respectively. These indicators testified to the strength of Thailand's export-oriented model, built on a diversified foundation of agriculture, industry, and services, including tourism.

Thailand's economic might was based on several key pillars. The country possessed developed infrastructure, from the modern Suvarnabhumi Airport to the region's largest Laem Chabang port. The industrial base included automotive, electronics, chemicals, and agricultural processing, ensuring stable export revenues to world markets.

However, even during this period, structural problems in the Thai economy were becoming apparent. Excessive dependence on external factors - tourist flows, global demand for industrial goods, and political stability - made the economy vulnerable to external shocks. Political instability, manifested in frequent government changes and periodic military coups, undermined long-term planning and investment attractiveness.

Vietnam's Rapid Rise

At the same time, Vietnam found itself in a completely different situation. In 2015, the country had a current account deficit of 2 billion dollars, while total export volume was only 162 billion dollars - 94 billion less than Thailand. However, it was from this moment that Vietnam's unprecedented economic breakthrough began.

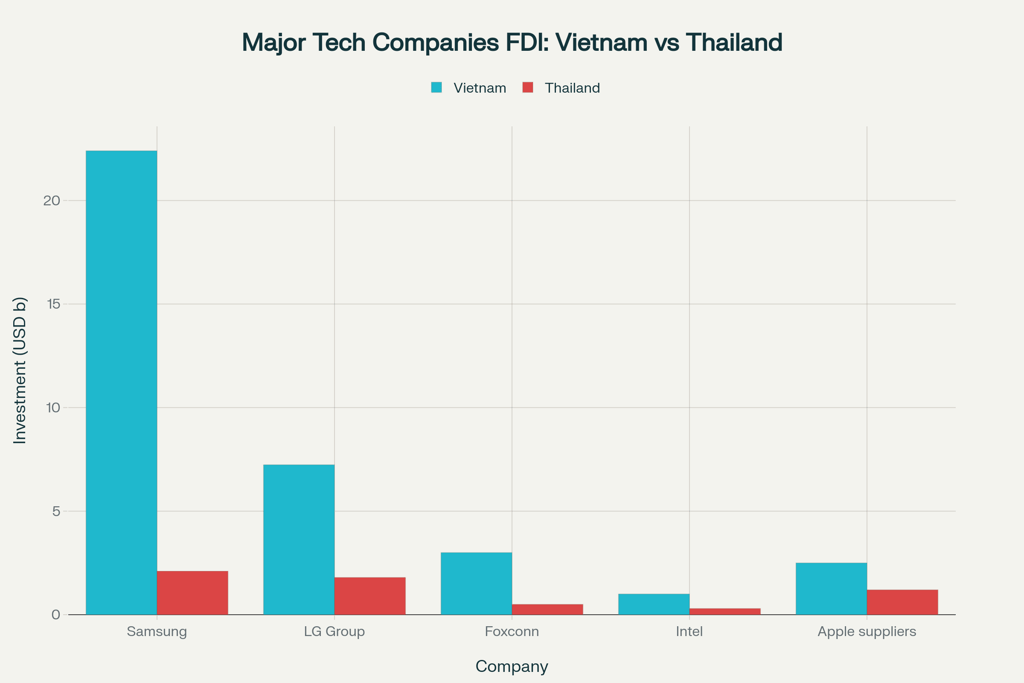

The key success factor was consistent implementation of a strategy to attract foreign direct investment (FDI) in high-tech industries. The world's largest technology corporations - Samsung, LG, Foxconn, Intel - invested billions of dollars in creating production facilities in Vietnam. Samsung alone invested 22.4 billion dollars in Vietnam, making it one of the largest foreign investors in the country.

Vietnam's geographical location proved to be a strategic advantage. Proximity to major Asian markets - China and South Korea - provided easy access to both component suppliers and finished product consumers. This is particularly important for the electronics industry, where delivery speed and logistics costs play a critical role.

Export Structure Transformation

From Textiles to High Technology

The most impressive aspect of Vietnam's economic miracle was the radical transformation of export structure. In 2015, the foundation of Vietnamese exports consisted of traditional industries - textiles, agriculture, and basic electronics. By 2024, the picture had changed dramatically: electronics became the dominant export item, comprising 126.5 billion dollars or 31.4% of total exports.

This transformation was not accidental - it resulted from targeted government policy to attract high-tech manufacturing. Vietnam's government created special economic zones with preferential tax regimes, invested in education and professional training, and concluded strategic free trade agreements that expanded access to world markets.

Major technology corporations played a key role in this transformation. Samsung turned Vietnam into its global production base, where the company's four factories generate about 30% of Samsung's global revenue and 33.5% of global profits. In 2023, Samsung Vietnam's export turnover reached 55.7 billion dollars, representing a significant share of the country's total electronics exports.

LG Group invested 7.24 billion dollars in seven major projects in Hai Phong province, including display manufacturing, electronics, chemicals, and international trade. Foxconn expanded its investments to 3 billion dollars, creating production facilities for Apple and other leading brands.

Comparative Electronics Export Dynamics

Electronics export statistics clearly demonstrate the scale of changes that occurred. In 2024, Vietnam exported electronics worth 126.5 billion dollars, 2.6 times exceeding Thailand's corresponding indicator of 48 billion dollars. Moreover, growth dynamics show steady expansion of Vietnam's sector: in the first quarter of 2025, computer and electronic component exports grew by 32.38% compared to the previous month.

The structure of electronics exports also demonstrates a high degree of specialization. Main categories include phones and components (53.9 billion dollars), computers and electronic components (72.56 billion dollars). This indicates that Vietnam has successfully integrated into global supply chains of the most dynamically developing technology sectors.

Comparative Analysis of Tourism Industry

Thailand's Traditional Leadership Under Threat

The tourism industry has long been Thailand's calling card and one of the key sources of foreign exchange earnings. In pre-crisis 2019, the country received 39.8 million international tourists, generating about 65 billion dollars in tourism revenue. However, the COVID-19 pandemic dealt a devastating blow to this sector, and recovery proved slower and more painful than expected.

In 2024, Thailand received 35.6 million tourists, which, while approaching pre-crisis levels, still remains below peak values. More alarming is the fact that 2025 shows declining tourist flows: in the first seven months, 19.29 million tourists visited the country, 6% less than the same period the previous year.

Thailand's tourism problems are complex. First, safety concerns cause serious worry. International incidents, including the kidnapping of a Chinese actress in January 2025, led to a sharp drop in confidence among Chinese tourists - traditionally Thailand's largest visitor segment. Second, the strengthening Thai baht made the country significantly more expensive for foreign tourists, especially from the middle class.

Vietnam's Rapid Tourism Growth

Against Thailand's difficulties, Vietnam demonstrates impressive tourism industry growth dynamics. In 2024, 17.5 million foreign tourists visited the country, representing a substantial increase compared to 12.6 million in 2023. The growth rate is particularly impressive: in 2025, Vietnam showed 21% growth in international arrivals, putting it on par with Japan as a country with the highest tourism growth rates in the world.

A key factor in Vietnamese tourism success was active "tourism diplomacy." The country's government conducted large-scale promotional campaigns in China, increased direct flights, and simplified visa procedures. Results were impressive: in the first quarter of 2025, Vietnam received more Chinese tourists (1.6 million) than Thailand (1.3 million) for the first time.

Geographic advantages also play an important role. Unlike Hainan, mainland China has few beaches suitable for swimming, making Vietnam's coastline particularly attractive to Chinese tourists. Additionally, mutual visa exemption, sister province agreements, and implementation of cross-border QR payment systems significantly simplified travel for Chinese citizens.

Structural Changes in Regional Tourism Competition

The leadership change in tourism reflects deeper structural changes. Modern travelers, especially the younger generation, increasingly seek unique, personalized experiences and emotional value, rather than simply visiting traditional tourist attractions. Vietnam successfully positions itself as a "fresh" destination with a combination of natural beauty, cultural heritage, and modern infrastructure.

Thailand, conversely, is increasingly perceived as an "outdated destination". Problems include deteriorating tourist facilities, unsatisfactory service quality, inadequate infrastructure connecting tourist cities, and changing traveler behavior. Competition from neighboring countries and other key destinations intensifies, especially considering China offers affordable prices and a wide range of products and services.

Macroeconomic Indicators and Structural Differences

Current Account Dynamics as Competitiveness Indicator

Comparing the current account dynamics of both countries clearly demonstrates cardinal changes in their relative competitiveness. In 2015-2016, Thailand demonstrated strong surpluses of 28 and 43 billion dollars respectively, while Vietnam had a deficit of 2 billion dollars. By 2024, the situation completely reversed: Vietnam's surplus reached 28 billion dollars, exceeding Thailand's indicator of 13.4 billion.

This transformation reflects fundamental changes in export sector competitiveness of both countries. Current account surplus exceeding 6% of GDP in Vietnam versus 2.5% in Thailand indicates that Vietnam's economy generates significantly more foreign exchange earnings relative to its size.

Economic Growth Rates and Their Determinants

Differences in economic growth rates are even more striking. In 2024, Vietnam's GDP grew by 7.09%, while Thailand showed modest 2.6%. Moreover, in the second quarter of 2025, Vietnam demonstrated growth acceleration to 7.96% - the highest since the third quarter of 2022.

These differences are due to structural factors. Vietnam's economy relies on dynamically developing high-tech industries integrated into global supply chains. Investments in education and professional training created a skilled workforce capable of serving modern production processes.

Thailand, despite higher development levels and GDP per capita, faces middle-income trap problems. Higher wages (431 dollars versus 342 dollars in Vietnam) make the country less attractive for labor-intensive manufacturing, while transition to high-tech industries occurs slower than in Vietnam.

Demographic and Social Factors

The demographic situation also plays an important role in economic dynamics. Vietnam's median population age is 30 years versus 40 years in Thailand. A younger population means higher productivity, stronger consumption, and greater adaptability to changes. Thailand, as one of ASEAN's most rapidly aging societies, faces rising healthcare costs and shrinking labor resources.

Role of Foreign Direct Investment and Technology Transfer

Scale and Structure of FDI in Vietnam

Foreign direct investment became the catalyst for Vietnam's economic miracle. Total FDI volume from major technology companies in Vietnam significantly exceeds similar investments in Thailand. Samsung invested 22.4 billion dollars in Vietnam versus 2.1 billion in Thailand, LG Group - 7.24 billion versus 1.8 billion respectively.

These investments are not just quantitative but also qualitative in nature. Companies create not only production facilities but also research centers, development centers, and complete technological ecosystems. Qualcomm opened a research center in Vietnam, and NVIDIA recently signed a strategic partnership with the government to create a data center and AI research center.

Formation of Technology Clusters

The distribution of technology companies across Vietnam demonstrates the formation of powerful industrial clusters. The northern region concentrates about 65% of foreign electronic companies, including Fuji Xerox, Compal, Canon, Foxconn, Samsung, Intel, LG Display, Panasonic, Luxshare, and many others. These companies locate in industrial zones of Hai Phong, Bac Ninh, Bac Giang, Thai Nguyen, and Ha Nam.

The southern region, including 30% of foreign electronic enterprises, is concentrated in industrial zones of Binh Duong, Ho Chi Minh City, and Dong Nai. Such geographic distribution creates synergetic effects where enterprises can use common supply chains, logistics infrastructure, and qualified personnel.

Technology Transfer and Production Localization

A crucial aspect of Vietnam's strategy was not simply assembling foreign components but gradual production localization and technology transfer. The government adopted a semiconductor industry development strategy until 2030 with prospects until 2050, marking a decisive step toward strengthening internal capabilities - from personnel training and production localization to active participation in research and production of key technologies.

Political Stability as Investment Attractiveness Factor

Impact of Political Instability in Thailand

Political instability in Thailand became a serious obstacle to long-term investment and economic planning. In 2025, the country again faced a wave of political protests demanding Prime Minister Paethongtarn Shinawatra's resignation. The Bhumjaithai Party's exit from the ruling coalition left the administration with a shaky parliamentary majority.

The impact of political uncertainty on the economy proved significant. Thailand's stock exchange index (SET) fell almost 24% since the beginning of the year, reaching its lowest level in over three years. Foreign investors withdrew more than 2.3 billion dollars from Thailand's stock market in 2025, as concerns about political risks and declining regional competitiveness intensified.

The Federation of Thai Industries (FTI) warned that political uncertainty damages both domestic and foreign investment confidence. Projects awaiting approval or construction start are particularly affected, many of which may be postponed indefinitely.

Advantages of Vietnam's Political Stability

Unlike Thailand, Vietnam demonstrates relative political stability, which is a key factor in attracting long-term investment. The one-party system ensures political course predictability and the possibility of implementing long-term economic strategies without risk of their cardinal revision during government changes.

This stability is particularly important for technology companies planning multi-billion-dollar investments in production facilities and research centers. A Chinese investor who recently invested over 100 million dollars in electronic component manufacturing in Vietnam cited improving investment environment and quality workforce as key factors for choosing Vietnam.

Integration into Global Trade Agreements

Vietnam's Strategic Trade Partnerships

Vietnam's success is largely due to active integration into global trade agreements. Over the past decade, the country signed more free trade agreements than any other ASEAN country, including agreements with the EU, UK, and CPTPP partners. The result was preferential access to over 60 markets and increased investment confidence.

Vietnam's participation in the Regional Comprehensive Economic Partnership (RCEP) and Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) provides significant trade advantages. RCEP, uniting 10 ASEAN countries and five trading partners, creates the world's largest trading bloc with 2.2 billion population and 30% of world GDP.

Thailand's Slow Integration

Thailand, conversely, demonstrated slower trade integration rates. Negotiations on a free trade agreement between Thailand and the EU, for example, remain unresolved. Political uncertainty and policy drift hindered strategic implementation of trade agreements. While Vietnam builds momentum, Thailand continues discussing development direction.

Production Costs and Competitiveness

Comparative Analysis of Labor Costs

One of Vietnam's key competitive advantages remains relatively low production costs. Average monthly wages in Vietnam's manufacturing industry are 342 dollars versus 431 dollars in Thailand. For labor-intensive manufacturing, this 21% difference can be critical in investment decisions.

However, it's important to note that Vietnam's advantage is not limited to low wages alone. Labor productivity in Vietnam is 85% of Thailand's level, meaning unit labor costs (wages adjusted for productivity) in Vietnam are significantly lower.

Energy and Operating Costs

Operating costs in Vietnam also remain more competitive. Industrial electricity costs in Vietnam are approximately 30% lower than in Thailand, which can lead to substantial savings for energy-intensive manufacturing processes. Industrial facility rent, administrative expenses, and other overhead costs are also typically lower in Vietnam.

Supply Chain Problems and Their Solutions

One traditional disadvantage of manufacturing in Vietnam was higher material and component costs due to the need to import them through multiple intermediaries. Materials costing 1 dollar in China could cost 3 dollars or more in Vietnam by the time they reached the factory. However, massive presence of major technology companies gradually solves this problem by creating local supply chains and attracting component suppliers.

Sectoral Specialization and Diversification

Concentration versus Diversification

A fundamental difference between the two countries' economic strategies lies in their approach to sectoral specialization. Vietnam concentrated on electronics, which comprises 41% of total exports (165 billion dollars in 2023). This concentration allowed achieving economies of scale, creating powerful industrial clusters, and maximizing synergetic effects between industry enterprises.

Thailand, conversely, maintains a more diversified export structure including electronics, machinery, tourism, agriculture, and chemicals. While such diversification should theoretically provide a more stable industrial base, under conditions of general weakening world demand, it makes Thailand more susceptible to negative trends in many industries simultaneously.

Evolution of Export Basket

Vietnam's export structure transformation demonstrates a classic example of successful export-oriented industrialization. The share of textiles and agriculture in exports decreased from 38% in 2015 to 28% by 2023, as the country transitioned to more advanced manufacturing. This transition reflects natural evolution of a developing economy from low value-added goods to more valuable products.

Regional Competition and Geopolitical Factors

Competition within ASEAN

The economic leadership change between Thailand and Vietnam occurs in the context of broader regional transformation. According to 2024 data, total ASEAN trade volume was approximately 3.5 trillion dollars, with 21.5% of trade occurring within the bloc. Vietnam ranked second in ASEAN export volume with 405.53 billion dollars, trailing only Singapore (504.87 billion).

Thailand dropped to fourth place with 300.5 billion dollars in exports, also falling behind Malaysia (330.04 billion). These changes reflect fundamental shifts in regional competitiveness and specialization.

Impact of Trade Wars and Geopolitical Tensions

The US-China trade war unexpectedly became a catalyst for Vietnamese economic growth. Companies seeking to diversify production and avoid American tariffs on Chinese goods actively relocated production facilities to Vietnam. Vietnam's political stability and security, combined with competitive costs, made the country a preferred location for such diversification.

Challenges and Prospects for Sustainable Development

Environmental and Social Aspects of Growth

Vietnam's rapid economic growth raises important questions about its sustainability from environmental and social perspectives. Concentration of heavy industry and electronics manufacturing creates significant environmental burden, including water and air pollution and electronic waste generation.

Vietnam's government recognizes these challenges and works toward their resolution. The semiconductor industry development strategy includes environmental sustainability and "green" growth requirements. International companies also implement environmental responsibility standards in their Vietnamese operations.

Risks of Excessive Export Dependence

The success of Vietnam's export-oriented model also creates certain risks. Excessive dependence on external markets makes the economy vulnerable to global economic shocks, trade wars, and changes in international trade policy. The recent agreement with the US to introduce a 20% tariff on Vietnamese imports (reduced from planned 46%) demonstrates the importance of diversifying trade partners.

Need for Domestic Market Development

For long-term economic growth sustainability, Vietnam needs to develop its domestic market and consumption. With a population exceeding 100 million and rising incomes, the country has significant potential for developing domestic demand. This is particularly important in the context of possible global economic growth slowdown and strengthening protectionist tendencies.

Lessons Learned and Regional Policy Implications

Importance of Consistent Economic Policy

Vietnam's experience demonstrates the importance of consistent and targeted economic policy. Unlike Thailand, where frequent government changes led to economic course modifications, Vietnam managed to implement a long-term strategy of attracting high-tech FDI and integrating into global supply chains.

Key elements of successful strategy included: creating attractive investment climate, investing in education and professional training, developing industrial infrastructure, active trade diplomacy, and concluding strategic trade agreements.

Role of State in Economic Transformation

Vietnamese experience confirms the important role of the state in directing economic transformation. The government not only created favorable conditions for investors but actively shaped development priorities, directing resources to strategically important industries and regions.

Creating special economic zones, targeted tax incentives for high-tech companies, investments in transport infrastructure and education - all these are examples of active industrial policy that contributed to the country's success.

Forecasts and Future Development Scenarios

Short-term Prospects (2025-2027)

In the short term, Vietnam will likely maintain its advantage over Thailand in key economic indicators. IMF forecasts suggest Vietnam's economic growth in 2025 will be 6.5%, significantly exceeding expected 2.7% for Thailand.

However, Vietnam may face certain challenges. The impact of American tariffs, though mitigated to 20%, may negatively affect exports. Additionally, base effects may lead to some growth rate deceleration as economy size increases.

Medium-term Prospects (2025-2030)

In the medium term, Vietnam's ability to maintain competitiveness amid rising wages and production costs will be critically important. The country must continue moving up the value chain, developing its own research and development, creating national brands, and increasing the share of high-tech services in the economy.

According to IMF forecasts, by 2029 Vietnam's GDP could reach 627 billion dollars, exceeding Thailand's projected 616 billion dollars. This would make Vietnam the world's 32nd largest economy and fourth in the region.

Long-term Challenges and Opportunities

In the long term, both countries will face common regional challenges: population aging, need for sustainable development transition, climate change adaptation, and managing production automation consequences.

Success will depend on ability to adapt to these changes, develop human capital, and maintain innovation potential. Vietnam has the advantage of a younger population but must invest in higher education and research. Thailand, possessing a more developed economy and infrastructure, can focus on high-tech services and innovative industries.

Conclusion: New Paradigm of Regional Development

The economic leadership change between Thailand and Vietnam represents not merely a statistical fact but a fundamental transformation of Southeast Asia's economic geography. This process demonstrates that under globalization and technological revolution conditions, traditional advantages - geographic location, natural resources, historical legacy - can be quickly neutralized by new competitiveness factors.

Key factors of Vietnam's success included: strategic planning and consistent economic policy implementation, active attraction of foreign direct investment in high-tech industries, successful integration into global supply chains, political stability, demographic advantages of young population, competitive production costs, and active trade diplomacy.

Thailand's difficulties are associated with political instability, higher production costs, slow adaptation to changing global conditions, tourism industry problems, and insufficient resource concentration on breakthrough development directions.

The experience of these two countries provides important lessons for other developing economies in the region and world. It shows that export-oriented industrialization can still be an effective development strategy with proper implementation, but requires constant adaptation to changing global conditions and consistent state policy.

In a broader context, this case illustrates the dynamism of the modern world economy, where countries' positions in the global hierarchy can change over a relatively short period. Success in these conditions requires not only economic policy but also strategic thinking capability, adaptation, and constant renewal of competitive advantages.

The future will show whether Vietnam can maintain high growth rates when transitioning to a middle-income economy, and whether Thailand will succeed in regaining lost positions through economic modernization and improved political stability. In any case, the transformation that occurred over the past decade has already changed Southeast Asia's economic map and will have long-term consequences for regional development.

https://www.vietnamexportdata.com/blogs/vietnam-electronics-exports-2025-data-report

https://thailand.prd.go.th/en/content/article/detail/id/2085/iid/358440

https://www.ceicdata.com/en/indicator/thailand/current-account-balance--of-nominal-gdp

https://www.ceicdata.com/en/indicator/thailand/current-account-balance

https://www.bangkokbank.com/th-TH/-/media/c16c2f5658b04f5cb1c345c908f0c284.ashx

https://www.aseanbriefing.com/news/thailands-political-protests-implications-for-foreign-investors/

https://delco-construction.com/en/the-wave-of-investment-in-the-electronics-industry-in-vietnam/

https://vietnamlawmagazine.vn/vietnam-destination-for-pioneering-industries-72300.html

https://the-shiv.com/vietnams-computer-and-electronics-exports-rise-by-32-38-percent-in-march/

https://forevervacation.com/the-vacationer/thailand-tourism-statistics-2024

https://www.statista.com/statistics/994693/thailand-number-international-tourist-arrivals/

https://marketresearchthailand.com/insights/articles/thailand-tourism-safety-concerns-market-trust

https://www.vietnam-briefing.com/news/vietnams-tourism-growth-policies-opportunities.html/

https://www.focus-economics.com/country-indicator/thailand/current-account/

https://www.aseanbriefing.com/news/southeast-asia-manufacturing-tracker/

https://en.vietnamplus.vn/electronics-industry-seizes-restructuring-opportunities-post322663.vnp

https://seasia.co/2025/08/27/asean-and-rcep-pioneering-regional-economic-integration

https://seapublicpolicy.org/southeast-asia-global-relations-outlook-part-5-international-agreements/

https://asia-agent.com/blog/cost-comparison-manufacturing-in-china-vs.-southeast-asia

https://www.tradeimex.in/blogs/top-asean-exports-trading-bloc-overview-2025

https://wtocenter.vn/chuyen-de/26835-thailands-economy-lagging-behind-that-of-other-asean-nations